Employee Private Tender Offers: what information do companies need to disclose?

(Originally published for Founders Circle on January 8th, 2018)

In order to conduct or facilitate a private tender offer, companies are often required to disclose confidential information they’re used to guarding closely. Because the potential sellers—usually employees—typically don’t have the same information as the buyer—usually a current institutional shareholder, a growth equity fund, or the company itself—executives are tasked with bringing them up to speed on the risks, financial health, and history of the company. That way the potential sellers can make an informed decision about the offer in front of them.

To comply with anti-fraud rules (SEC Rule 10b-5), it’s important to close any material information gap between the buyers and the sellers. Yet while there are some basic anti-fraud rules that apply to all securities transactions, there’s limited guidance when it comes to private tender offer rules. The good news is that following some best practices during a private liquidity program can help protect the company from liability down the line while keeping sensitive information secure.

We asked James Hutchinson and Cameron Contizano of Goodwin Procter LLP to give us some insight into these disclosure practices. Hutchinson orchestrated the first pre-IPO employee private liquidity transaction at Facebook (structuring discussions that were held in Mark Zuckerberg’s living room). Contizano has extensive experience organizing secondary transactions, including a tender offer for Twilio.

The conversation has been edited for length and clarity.

Why is disclosure important in a secondary transaction?

Hutchinson: In private liquidity programs, you’re trying to give buyers and sellers the information they need to make an informed investment decision. While many employees can be exceptionally smart in their field of expertise, they can sometimes be unsophisticated in financial matters.

Imagine a seller that’s a 24-year-old engineer at a big tech company, and the buyer that’s a venture firm with a board representative—that’s a challenge from an information disclosure perspective. The buyer likely has a lot of information about the company’s finances and overall prospects and the seller might have very limited information of that sort. From a legal and fairness perspective, the worry is that an employee could come back long after the secondary transaction when a company sale or IPO is occurring at a higher price and say, “Hey, I didn’t have enough information to make an informed decision and would have waited to sell.”

Contizano: The employee could sue, or threaten to sue, to unwind the earlier secondary sale. That’s a terrible result from the company’s perspective because it puts a cloud on who actually owns the company’s stock. And if the company plans to go public or sell, nothing will spook an underwriter or buyer more than disputes over the cap table.

Has this ever happened?

Hutchinson: There was a case a couple years ago, the Stiefel Labs case, where the SEC brought an enforcement action against the board. The company was buying shares from employees when the board of directors knew the company was being sold at a much higher price than was being offered to the employees. That case was particularly egregious, but even companies like Facebook that worked very hard to ensure securities law compliance had lawsuits between buyers and sellers.

The government has been keenly focused on this to make sure things are done properly. That’s why you see a fairly formalized and structured approach to disclosure in private tender offers which is to ensure the parade of horribles don’t happen.

What are the best practices for disclosure?

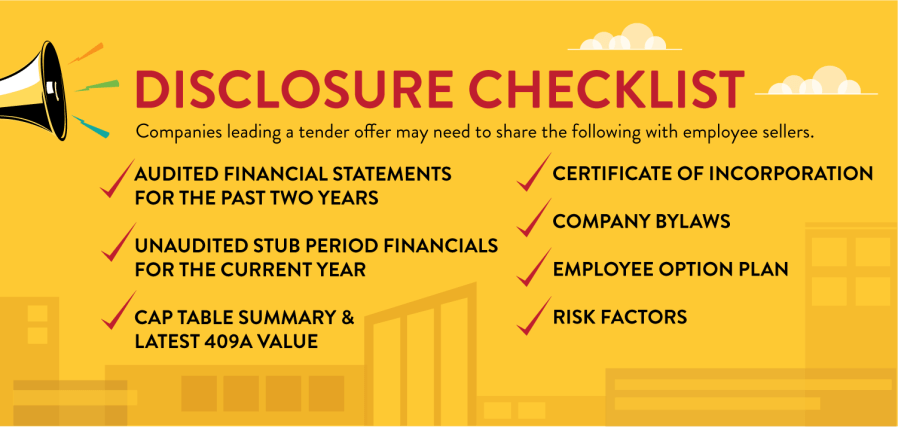

Contizano: Companies generally provide two years of audited financial statements. If they don’t have audited numbers, they provide unaudited. Then, if the tender offer is in June, for example, they provide stub period unaudited financials for the first two quarters. It’s become customary in secondary transactions to provide a high-level summary cap table (along with the latest fair market 409A valuation of common stock) in order to give people an idea of how many shares are outstanding in the company and the ability to calculate their percentage ownership. We also recommend in any private liquidity program that the company’s charter or operating agreement, bylaws and, if employees are sellers, the applicable employee option plan also be provided.

Hutchinson: Then there are risk factors. They cover a bunch of topics, including the risks of the business and the industry, the risks of not selling your stock and the risks of selling it. For example, there will be disclosure for sellers that make clear, “there’s no guarantee that there will ever be another opportunity to sell your shares.” So that’s a risk of not selling. But then there’s another disclosure that says “we might be sold or do an IPO in the future and the company’s shares could sell at a higher price than is being offered now.”

Then there’s a set of risk factors about the company. For example, if the revenue is highly concentrated from two big customers, if the company loses one of these customers, it will substantially impact the business. Or if the company is heavily reliant on IP, a patent troll could affect the business. Many are qualitative, but there can be some quantitative like we have $10,000,000 of cash left and if we don’t raise another round, we’ll run out of money in six quarters.

Is there any information that a company doesn’t need to disclose?

Hutchinson: The important question to ask is: what’s material? Specific monthly operating metrics or a small litigation with a former vendor can be the sort of things that on their own just aren’t very important when making an investment decision. But if there were bet-the-company IP litigation going on, information of that sort could be quite material. You have to strike a balance between giving people the material information but not overwhelming them with the minutia. There’s no clear answer and that’s where lawyers and business people have to make judgment calls.

What about projections?

Hutchinson: Projections can be one of those areas where a judgment call needs to be made. Many consider long-term projections to be so uncertain (i.e. someone’s best guess) that they aren’t actually deemed material. But disclosure regarding current or near-term trends regarding financial performance have become more commonplace.

Contizano: We’re starting to see more companies do something similar to “management discussion and analysis” as part of liquidity program disclosure. It’s something public companies do routinely. It’s a section in the offer documents written in plain English prose describing the basic financial performance and near-term performance trends.

What are the risks with disclosure?

Hutchinson: A private company has a number of very legitimate and important reasons to not want all sorts of information, including its financial statements, made public. We’ve seen instances where competitively sensitive information the CFO and CEO don’t want to be made public gets leaked within a short period of time after the launch of a private liquidity program. But fortunately, new technology can help.

Contizano: Some things have been done to keep information secure. A number of years ago, high profile “unicorns” would make financial statements available only in hard copies in the general counsel’s office and you had to get permission to review the materials. Nowadays, everything is usually available in an online platform and you have to log in to see it. Materials are watermarked and you can’t print or download documents. If you take a screenshot, it has your name and email address on it. Everybody would be able to figure out who let the cat out of the bag. But like many things, it’s not entirely bulletproof.

What are the best practices when communicating all this company information to employees?

Hutchinson: Bigger, more sophisticated companies hold town halls. There’s an explanation of the transaction process itself, from getting the invitation to participate over email to filling out the forms and guidance on how to sell shares on the platform. Often companies will have a dedicated email address where potential sellers can ask questions and receive answers from in-house stock administrators or insider or outside counsel.

Most companies really want these programs to be successful and to reward employees for their hard work. We’ve even seen companies invite outside financial advisors to hold “office hours” so employees with less financial sophistication can ask questions and get advice.

One of the things the private tender offer rules do require is that the offer to sell remain open for 20 business days. This typically provides sellers with plenty of time to look over the information, ask questions, make a decision and then sell if they wish.

Contizano: I do feel like companies today are trying to be more transparent generally about the big things that are happening in the company. The market has really moved in that direction the last 10 years. Companies seem to be more willing to share information on an ongoing basis with people who are actively contributing to the company’s success. That shift, plus technology like that provided by Nasdaq Private Market to facilitate these transactions, have made it less burdensome for companies to make confidential disclosure materials available.

This is a lot of work. Are there situations where it isn’t worth doing a secondary transaction?

Hutchinson: If you have less than 10 or so sellers sometimes the legal and process requirements for a private liquidity program are not really worth the administrative effort. In those situations, companies may still want to reward employees but decide to just give a cash bonus or some other incentive. If they do that, companies don’t have to comply with complicated securities rules and associated disclosure. Or the company can facilitate individual secondary transactions instead of a full-blown tender offer, depending on the circumstances.

For a bigger private company, a private liquidity program can make sense for them because it’s a really good recruiting and retention tool for employees. You’re telling employee sellers, “you don’t have to wait for an IPO to see value for your options. We can give you cash now for your stock options or shares. You don’t have to go work for a large public company to get liquidity.”

What’s your best advice for companies putting together disclosure materials for a secondary transaction?

Hutchinson: Get good legal advice but also put yourself in the shoes of that 24-year-old engineer that may not have a ton of financial experience yet. (Sellers and third-party buyers should consider getting their own advice, too.)

Contizano: The other thing I’d say is don’t rush it. Think about it a little bit. We see companies wanting to launch a private liquidity program really fast but they haven’t taken the time to really formulate the “rules” of the tender offer (e.g. who can sell and how much) or properly prepare the disclosure materials. That’s where mistakes get made. Instead, just step back and do a little more planning upfront. It will make the process go more smoothly and there will be less chance of having to make changes to the offer documents or disclosure materials during the offer period to correct something that wasn’t thought all the way through at the outset.